It can definitely be stressful trying to figure out what to do when you need to get some money fast, especially when traditional lenders just won’t cut it. I felt that way when I was trying to get a commercial real estate project started. I was going to buy a property that was slightly distressed, so no traditional lenders would lend to me. It was at that moment that I started to learn about hard money lenders.

One of the first lenders I found during my research was called Kennedy Funding. They said that they could lend to me and do so quickly. They said that they would be able to solve my problems. They, however, did not live up to that reputation. I began uncovering a trail of frustrated borrowers, leading me straight down the rabbit hole of the Kennedy Funding ripoff report phenomenon.

There were so many other stories of people in extreme financial situations. I decided to track down a case that became really financially litigated, and that was my case against Kennedy Funding.

Today, I want to discuss these findings with you. I want to discuss the lessons that I have learned the hard way, and the other people who have also learned these lessons the hard way. All of this is going to be about the lawsuits, the fees, and the lessons about Kennedy Funding that people had to learn the hard way.

Table of Contents

Who Exactly is Kennedy Funding?

Before diving into the specifics of the complaints, some context is helpful. Kennedy Funding, based in New Jersey, claims to be a leading direct private lender. They tend to focus on the types of deals that give traditional bank underwriters a cold sweat: commercial real estate, distressed real estate, raw land, and even overseas real estate.

In the business world, they are known as lenders of last resort. They are the ones with the checkbook when you don’t know where else to go. But here’s the catch: being a last-resort lender costs a lot of money. It’s like buying a bottle of water in the desert: you’ll have to pay a lot more because you don’t have any other choices.

Unfortunately, for many borrowers, this extra cost wasn’t just high interest rates. It also included practices that led to a lot of Kennedy funding complaints.

The Anatomy of a Kennedy Funding Ripoff Report

As you start sifting through multiple reports and reviews, you begin seeing a pattern. The reason for looking up a Kennedy Funding Ripoff Report is typically to figure out one thing. Is this a Scam or just a really bad business deal?

Here is a summary of some of the more commonplace criticisms I’ve come across in my research.

The Pitfall of Upfront, Non-Refundable Fees

Kennedy Funding is a Clear Example of a Legal Scam. It’s like walking into a car dealership, paying a ‘test drive’ charge of $10,000, and then not being allowed to purchase the car and having the charge for the test drive permanently retained.

Numerous potential borrowers have reported being charged for large, mandatory, non-refundable, up-front ‘due diligence’ or ‘commitment’ fees. The problem?

These fees are claimed to be retained regardless of whether or not the loans are closed. Critics claim the firm uses vague, value definitions pertaining to some pieces of collateral to ensnare the more desperate borrowers into counterproductive contracts and then pulls the rug out from under them to keep the money.

Bait-and-Switch Loan Terms

One of the key pillars of the complaints involves the deceptive loan terms. Numerous borrowers are reporting that the terms that were presented to them and that convinced them to pay those large, hefty upfront fees changed significantly right before the closing.

The sizes of loans were suddenly decreased, and the terms of the payments were changed. This is textbook bait-and-switch, leaving borrowers desperate after having invested thousands of dollars into the process.

Spot the Trap: Professional vs. Predatory Lending

| The Situation | What’s Professional? | What’s a Red Flag? |

| Initial Deposits | Fees cover only 3rd party costs (Appraisal). | Large Commitment Fees before a term sheet. |

| Loan Terms | Terms remain consistent with the offer. | Sudden changes in loan size at the final hour. |

| Communication | Proactive updates and clear timelines. | Total Radio Silence after fees are paid. |

| Valuation | Based on fair, independent market data. | Using internal low-ball values to keep deposits. |

| Exit Strategy | Transparent points and clear exit costs. | Hidden penalties that trap you in the loan. |

3. The Communication Black Hole

When you are dealing with millions of dollars and tight real estate deadlines, communication is everything. Yet, a recurring theme in these reports is the sudden radio silence from the lender once the upfront fees are paid. Borrowers describe delayed responses, vague explanations, and a general lack of transparency that turns a stressful financial situation into an absolute nightmare.

Diving Deep into the Kennedy Funding Lawsuit Landscape

When you see the start of court proceedings, you know things have progressed far beyond a simple case of customer dissatisfaction. What is most concerning is the amount of litigation involving this company. Every Kennedy funding lawsuit I examined left me with the same impressions of claims involving predatory lending and unfair practices.

A legal dispute that stood out to me was Quimera Holding Group SAC v. Kennedy Funding Financial LLC. This case has a good representation of the main issues that borrowers tend to face. In the court documents, it was stated that the plaintiffs’ case against the firm was about the firm failing to honor loan commitments.

In 2025, a court found that Kennedy breached a loan commitment by making an offer that was under the required amount.

Domestic borrowers are not the only ones who feel the pain. Kennedy Funding has a broad scope that includes South America, Canada, and the Caribbean. This has spawned several complex cross-border litigations. Overseas construction companies have sued the company, arguing that they were misled regarding the repayment timelines and the rigid loan security requirements.

The Broader Kennedy Funding Controversy

How does this affect the market at large? The Kennedy Funding Controversy is more than a controversy; it is a reminder of the predatory practices that are often associated with the hard money lending market.

Generally, the courts are quite lenient with private lenders.

The courts recognize the fact that anyone involved in commercial real estate is a sophisticated business person and knows how to interpret a contract. The distinction between hardball business terms and illegal predatory lending is very thin.

Most lawsuits against private lenders only succeed when borrowers prove misrepresentation or fraud, or terms so unconscionable that they shock the legal conscience or violate state anti-usury laws.

This controversy has sparked a ripple effect. State regulators are beginning to look more closely at private lenders, considering more stringent regulations to protect borrowers. Furthermore, it has empowered borrowers. Seeing others stand up to these practices encourages new borrowers to challenge unfair terms rather than just accepting a terrible contract as gospel.

My Personal Takeaways: Lessons for Borrowers

Looking back at my own journey, I am incredibly grateful I didn’t let my desperation blind me. I walked away from the hard money route and eventually found a local credit union willing to work with me through a specialized SBA program. It took longer, but it saved me from potentially becoming another statistic in a lawsuit.

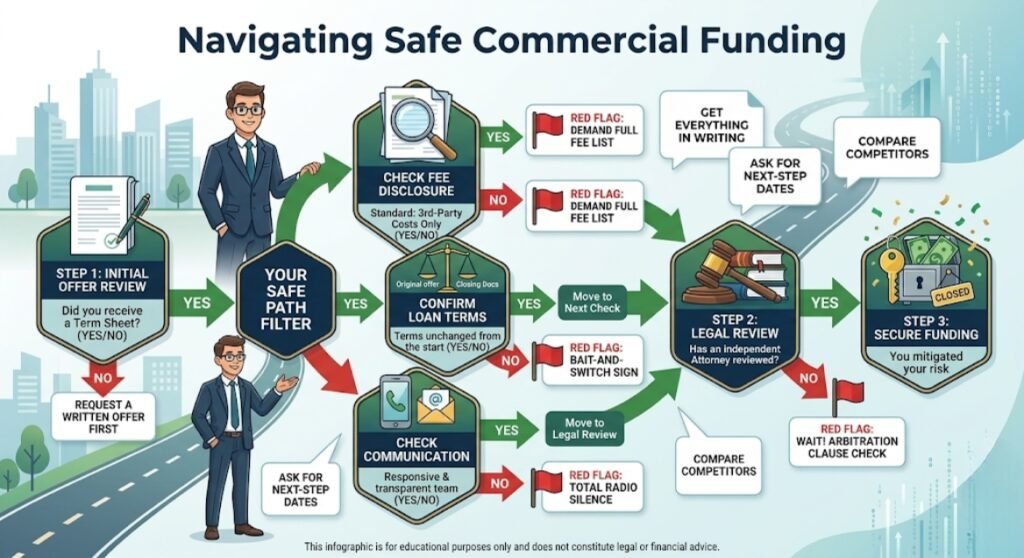

Note: This infographic is for educational purposes and reflects general industry safety standards; it is not a substitute for professional legal advice.

If you are currently considering a private lender, whether it’s Kennedy Funding or anyone else, please take these lessons to heart:

Strategic Alternatives: Choosing the Right Lifeline

| Funding Route | Best For… | The Main Benefit | The Trade-Off |

| Hard Money | Distressed assets / Last resort | Lightning-fast closing | High risk & massive fees |

| SBA / Credit Unions | Stable businesses & growth | Government-backed safety | Slow approval process |

| Private Equity | Large-scale developments | Flexible, partner-style terms | High equity requirements |

| Bridge Loans | Short-term financing needs | Fills the gap between deals | Requires a solid exit plan |

Frequently Asked Questions

Q. What exactly is a hard money loan, and why do companies like Kennedy Funding offer them?

A hard money loan is a type of financing secured by real estate. Unlike traditional bank loans, they are typically issued by private investors or companies. Lenders offer them to borrowers who may not qualify for conventional loans due to poor credit or the property’s condition. In exchange for taking on this higher risk, lenders can charge significantly higher interest rates and fees.

Q. Can private lenders legally charge non-refundable upfront fees?

Legally, this depends on the specific language in the contract and the state laws governing the transaction. While non-refundable fees are common in commercial lending to cover the lender’s underwriting and appraisal costs, courts have sometimes ruled against lenders if the fees were obtained through deceptive practices, ambiguous terms, or if the lender never actually intended to fund the loan.

Q. How can I verify if a private lender is legitimate before paying any fees?

First, verify the lender’s licensing through your state’s Department of Banking or Financial Regulation. You should also check their Better Business Bureau (BBB) rating and search public court records for any history of litigation. Finally, ask the lender for references from past borrowers who have successfully closed loans with them.

Q. What should I do if I think I’m a victim of predatory commercial lending?

First, consult with a commercial litigation attorney who specializes in real estate and finance. You can also file a complaint with your state’s Attorney General’s office and the Consumer Financial Protection Bureau (CFPB), although the CFPB primarily handles consumer loans rather than commercial ones. Document all communications and financial transactions meticulously.

Conclusion

The saga of Kennedy Funding is a cautionary tale about the clash between desperate borrowers and aggressive, opportunistic lenders. For a select few, this company may have provided the life-saving capital needed to finish a project. But for far too many others, it resulted in suffocating debt, lost upfront fees, and years tied up in stressful litigation.

When you read a Kennedy Funding ripoff report, you aren’t just reading a bad Yelp review; you are reading a warning sign. The high-stakes universe of commercial lending is unforgiving. Arm yourself with knowledge, retain excellent legal counsel, and never let financial desperation push you into a deal that your gut tells you is wrong.

Additional Authentic Resources

To further your research and ensure you are making the safest financial decisions, consider exploring these reputable resources:

{kind=link}